Articles Tagged: debt

Owning a Beater Car

There is something to be said for a beater car. And these days, buying a new car is a luxury.

The No Worries Way

I am in New York for the launch of No Worries. Let’s talk about all the personal finance decisions I made to get here.

Points and Miles

Here is the thing with miles and points: People spend a lot of mental energy trying to figure out how to get the miles and points, and then they get the miles and points but never use them.

New Year’s Resolutions, Etc.

Some people get themselves in a big financial jam, like with six figures in credit card or other debt. Then they feel stuck—it will take a decade to pay this off. It is pretty close to checkmate.

Buying a House in Today’s Interest Rate Environment

Even if you’re not up to your eyeballs in the financial world, you have probably heard that interest rates have come down a bit. Ten-year interest rates have dipped about 1%. Thirty-year fixed-rate mortgages are benchmarked off 10-year interest rates, so mortgage rates have come down about 1%.

You Have to Get These 7 Big Money Decisions Right

A lot of people are stressed out about money.

This leads them to take on lots of debt or too much risk in the stock market. Then those stupid decisions ramp up their financial stress even more.

People call my radio show to ask about money and investing. But I didn't create this show to help people make more money. My goal is to help people focus on being happy.

I'm plenty happy—don't let my resting unhappy face fool you. That's because I live a stress-free financial life.

Here's how I've done it… and how you can too.

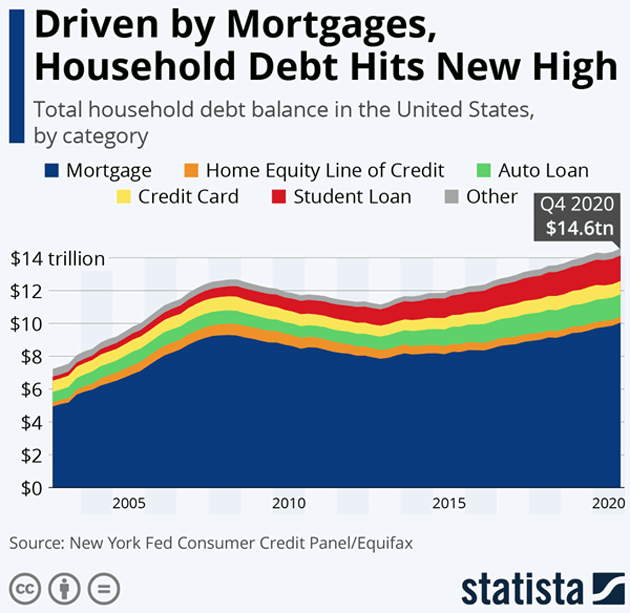

1. Minimize your debt

Eighty percent of Americans carry some type of debt. And they pay 20% of their income to service that debt.

When you write out your $2,000 mortgage check, for example, you pay $400 in principal. The other $1,600 is the bank's profit.

Source: Statista

You don't want to be a good bank customer. You don't want to be a customer at all.

Interest is the penalty you pay for getting money now instead of later. And if you're the one doing the lending to a friend or family member, you should charge interest.

2. Live within your means

Now, I’m not anti-spending. You can spend money. Just don't make it a competition.

So what if one neighbor has a new BMW and another has a Mercedes. Don't look at your Toyota and think you need a nicer car just to live in your neighborhood.

If your Toyota's payments are low or you've paid off that loan, smile at "The Joneses" as you drive by.

After all, they might just be part of the 80% who are sitting on a pile of debt.

3. Get the big things right

I'm talking about your car again. This one also includes your house and student loans.

Look, you don't create wealth by turning off your lights or thermostat. That 50 cents you save baking bread instead of buying it isn't going to change your life.

What does count are the big decisions you make in life.

-

Did you buy a house you can afford? Or are you stuck with a huge house and a huge mortgage?

-

Did you get a car you can afford? Or are you stuck with big payments, high interest, and expensive repairs?

-

Did you get your student loans right? If you took out $200,000 when you were 18, you're probably having a tough time.

If you went too big, that's what can screw up your financial position. You can't bake enough bread to finance those debts.

4. Invest early and often

Ideally, you want to start saving 20% of your income at age 22. If you don't have kids or a mortgage yet, save even more.

If you start investing when you're 40, you probably have to put aside 50% of your paycheck.

Whatever your age or financial position, get a 401(k), open an IRA, and start saving till it hurts.

It will hurt a lot more if you don't.

5. Get the asset allocation right

Everybody likes stocks these days. The market has been doing really well.

That won't always be the case. And a retirement portfolio that is 100% stocks will cause you a great deal of stress.

Even in a rising market like this one, you need to own other kinds of assets. I’m talking about things like gold, real estate, bonds, and cash. Otherwise, you're going to have a volatile portfolio.

Too much volatility makes people make stupid decisions. It's what made people sell their stocks when the markets went down last March… they couldn't stomach all that risk.

So, when you get that balance right (here's how)… you'll slash your financial stress.

6. Retire as late as you possibly can

Retiring early can destroy your finances and make you miserable.

If you retire at 58, you're going to have to stretch your savings out for 30 years. Most people don't save enough for the math to work out.

Sure, you can start taking Social Security as soon as you're eligible. That is, if you're OK with collecting teeny, tiny payments till you're 100.

Wait until you're 70 to take Social Security, if you can. The breakeven age is 74, and life expectancy is 80.

People tend to live longer than they think they're going to. And it's more fun if you're getting paid to do work you love.

7. Relax

Don't stress about becoming financially stress-free. Create your plan and stick to it, and everything is going to turn out fine.

-

What you invest in, is less important than the fact that you are investing.

-

What car or house you own, or what neighborhood you live in, is less important than being able to afford and therefore enjoy it.

-

Baking your own bread won't make you rich. Putting money in a bank account will.

There are plenty of other things to stress out about. Money shouldn't be one of them.

Jared Dillian

|

“Screw You!” Money Is Your Key to Freedom

No, I’m not being crass. This is serious stuff. If you want to experience true financial freedom, you need to make enough money to essentially say, “Screw you!”